Electric vehicle sales hit 17 million units globally in 2024, up 25% from 2023. The US crossed 1.5 million for the first time. China sold over 11 million EVs in 2024, accounting for nearly half of all car sales in the country.

Automakers made ambitious bets. Mercedes-Benz planned to produce only electric vehicles by 2030. General Motors aimed to follow by 2035.

Both have since reversed course.

>> Mercedes now expects only 50% electric and hybrid sales by 2030 and will continue making combustion engines "well into the 2030s."

>> GM maintains its 2035 electric-only goal but missed its 2025 production targets and is reintroducing plug-in hybrids by 2027.

The retreat reveals a fundamental problem: the transition hit a materials wall.

Road transport accounts for more than 15% of global energy-related emissions. Electrifying it is central to every net-zero scenario, and by 2025, global EV sales are projected to exceed 20 million units, representing more than one-quarter of all cars sold worldwide.

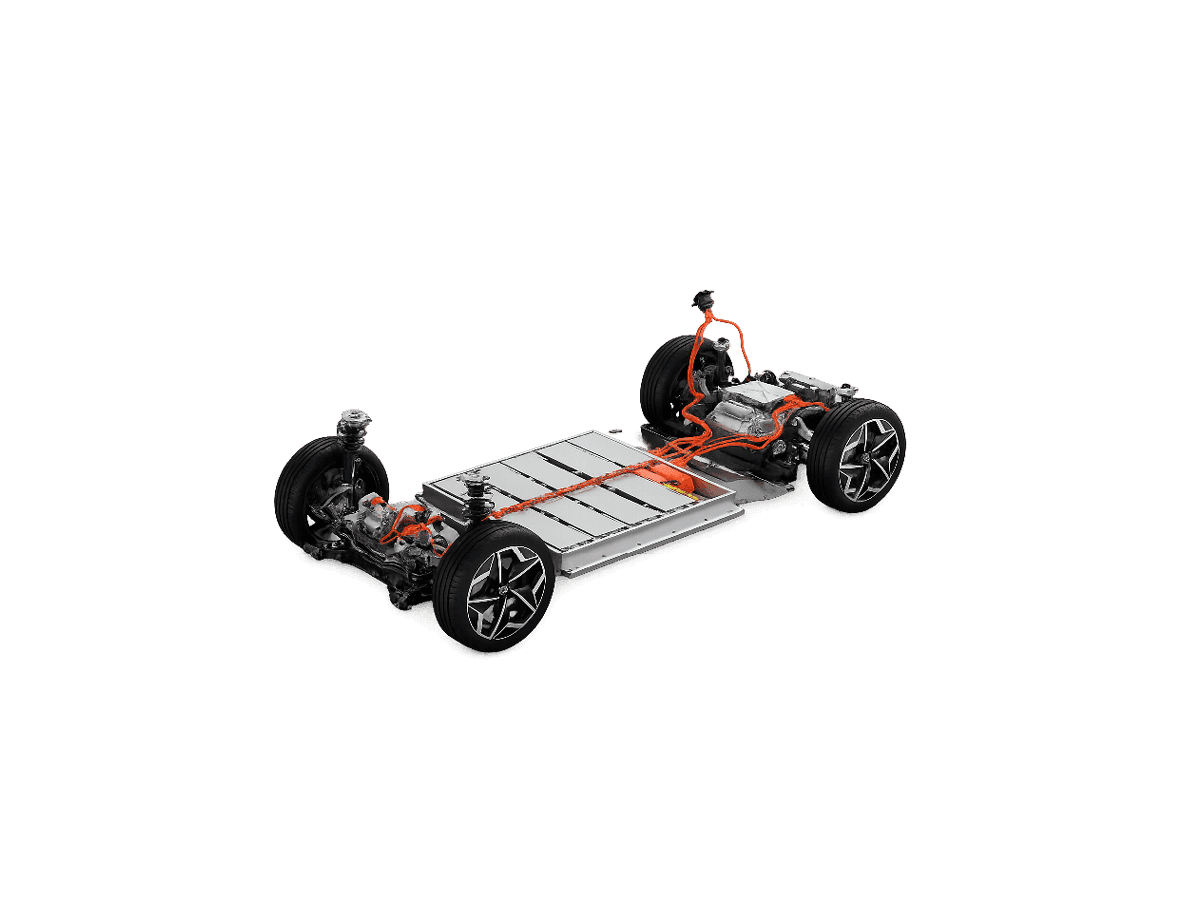

Then came "Battery Bloat'.

This was a Catalyst Nobody Planned For. Battery Bloat across the industry means that EV batteries are getting bigger and require more lithium.

An EV battery contains around 8 kilos of lithium. Scale that to tens of millions of electric vehicles sold in coming years, and EV batteries could absorb more than 90% of the lithium supply by 2030.

The energy transition stopped being just a technology problem and added a materials problem.

The "lithium paradox" is that although there is a lot out there, there may not be enough.

Lithium scarcity looks odd at first glance. Lithium is the 25th most abundant element in the earth's crust.

The problem is, it's not concentrated in easily extractable deposits the way that oil, gold, or natural gas are.

The United States Geological Survey estimates that there are approximately 86 million metric tons of identified lithium resources globally. But only one-quarter is economically viable to mine.

Elon Musk has been talking about this bottleneck for years. The limiting factor on how fast the world can transition to sustainable energy is the rate at which we grow battery production:

"There is no raw material constraint. Lithium is one of the most common elements on Earth. It's not so much the raw materials as it is converting the raw materials into the highly purified form that can be used in batteries. A tremendous amount of processing needs to happen, at scale comparable to the world oil and gas industry."

The Problem

Global lithium demand is forecast to reach 2.4-3 million tonnes by 2030, up from around 1.15 million tonnes in 2024. Leading analysts predict supply deficits ranging from 300,000 to 768,000 tonnes by 2030, even if every announced project comes online.

Only a fraction of identified lithium resources are economically viable to mine. Converting raw lithium into battery-grade material requires industrial capacity comparable to the oil and gas system that the energy transition is meant to replace.

That capacity does not yet exist.

Insatiable demand for lithium creates an urgent need for increased mining. That in turn will require a huge increase in investment in lithium mining projects. The lithium industry needs an estimated $42 billion in new investment to meet 2030 demand.

Physics > Platitudes

Europe is learning harsh lessons on the dangers of policymakers setting targets without understanding the limits imposed by physical reality.

The EU's proposed ban on sales of new petrol and diesel cars by 2035 was projected to create a five-fold surge in demand for lithium by 2030 to 550,000 tonnes per year.

Brussels set the deadline before anoyone checked if that amount of metal could relistically be mined.

The region's production capacity will be only 200,000 tonnes, indicating a shortage that threatens to derail Europe's EV transition.

This also represents potentially existential risk to the European auto industry, which cannot electrify future fleets without access to reliable and affordable lithium supplies.

Without that 350,000-tonne gap filled, assembly lines go dark and Chinese battery makers control the European market.

The stakes are clear: Whoever controls lithium controls the pace of electrification.

China Is Winning

The energy transition is not an abstraction that lives in spreadsheets and reports. It is physical. Lithium must be dug out of the ground, processed in refineries, and converted into battery-grade material through chemical treatments that take months.

China controls roughly 60% of global lithium refining capacity. Chile and Australia account for most of the remainder. The United States and Europe combined refine less than 3%.

The Inflation Reduction Act is a catch-up play. It encourages reshoring and friend-shoring, relocating processing back to the US and to geopolitical allies like Canada, Mexico, Australia, and Chile.

Bridging the lithium gap is now a prerequisite for the transition itself. The outcome will not be determined by forecasts or targets, but by which systems can secure, process, and sustain access to the underlying materials.

The race is on to develop lithium deposits and build out resilient supply systems.